Continuous probability distribution

Weibull (2-parameter)|

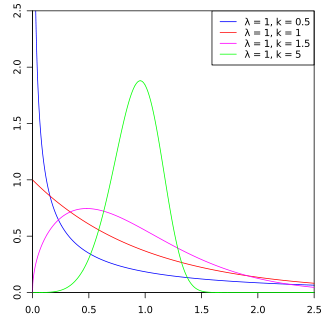

Probability density function  |

|

Cumulative distribution function  |

| Parameters |

scale scale

shape shape |

|---|

| Support |

|

|---|

| PDF |

|

|---|

| CDF |

|

|---|

| Quantile |

|

|---|

| Mean |

|

|---|

| Median |

|

|---|

| Mode |

|

|---|

| Variance |

![{\displaystyle \lambda ^{2}\left[\Gamma \left(1+{\frac {2}{k}}\right)-\left(\Gamma \left(1+{\frac {1}{k}}\right)\right)^{2}\right]\,}](https://wikimedia.org/api/rest_v1/media/math/render/svg/55fa6b5cdbe81bb9e6aa0452a2c619623cb23f14) |

|---|

| Skewness |

|

|---|

| Excess kurtosis |

(see text) |

|---|

| Entropy |

|

|---|

| MGF |

|

|---|

| CF |

|

|---|

| Kullback–Leibler divergence |

see below |

|---|

In probability theory and statistics, the Weibull distribution is a continuous probability distribution. It models a broad range of random variables, largely in the nature of a time to failure or time between events. Examples are maximum one-day rainfalls and the time a user spends on a web page.

The distribution is named after Swedish mathematician Waloddi Weibull, who described it in detail in 1939,[1] although it was first identified by René Maurice Fréchet and first applied by Rosin & Rammler (1933) to describe a particle size distribution.

- ^ Bowers, et. al. (1997) Actuarial Mathematics, 2nd ed. Society of Actuaries.